Even with rapid growth in online banking and mobile deposits, paper-based banking tools still play a major role in daily finance workflows. A 2025 Deloitte banking study showed that in-branch bank deposits remain common among small businesses and firms that regularly manage coin, note, and check-based revenue.

This is why structured tools like deposit slips and secure transport methods still matter. They help maintain accuracy between internal records and bank submissions. This guide shows how to fill out a deposit slip correctly and reduce risks during handling and transport with tamper-evident deposit bags solutions.

Why Commercial Businesses Still Need Physical Deposit Slips

While mobile banking apps easily process single checks for remote deposit capture, they possess severe operational limitations for commercial business models.

Understanding these digital bottlenecks explains why physical branch infrastructure and paper documentation remain completely irreplaceable for corporate treasury management.

- The Cash and Coin Handling Bottleneck: Mobile applications cannot process physical currency. For retail and manufacturing firms generating high volumes of cash daily, a physical deposit slip is the only mechanism to legally record physical cash ledger entries.

- Strict Digital Velocity Limits: Commercial banks enforce rigid daily dollar caps on mobile deposits to mitigate fraud risks. For businesses routinely exceeding these digital limits, attempting to use a mobile app halts daily cash flow logistics.

- Batch Control and High Volume Error Rates: Scanning individual commercial checks via smartphone is an error-prone and labor-intensive process. A physical deposit slip acts as an efficient batch control sheet, allowing teams to bundle large groups of checks under a single verified subtotal.

When your daily corporate revenue relies on secure, unlimited capital movement, filling out a physical deposit slip and utilizing an armored or secure tamper-evident transit system remains the only compliant option.

The Essential Components of a Bank Deposit Slip

A deposit slip is a foundational auditing tool in every commercial bank deposit process. It helps corporate customers and account holders organize loose cash and checks into highly structured deposits.

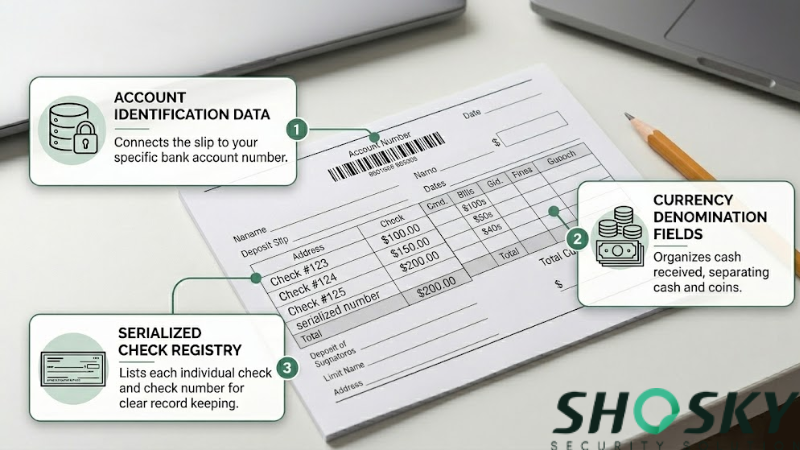

A standard deposit slip includes 3 main structural parts that guide accurate deposits and eliminate reconciliation errors.

- Account Identification Data: Connects every deposit slip directly to the correct corporate bank account number, ensuring deposit funds reach the exact account without institutional delays.

- Currency Denomination Fields: Organizes physical cash received by strictly separating notes and coins, which accelerates teller processing and supports accurate cash amount reporting.

- Serialized Check Registry: Lists each individual check and the corresponding routing check number, helping account managers track check deposits and maintain a clear audit trail.

Each component of a deposit slip plays a direct role in keeping financial records structured and exceptionally easy to verify. These details also support strict compliance with federal reporting requirements regarding commercial revenue documentation.

Step by Step: How to Fill Out a Commercial Deposit Slip

Filling out a commercial deposit slip requires careful attention at each stage to keep bank deposits completely accurate and seamlessly aligned with internal corporate records.

When financial officers or account holders fill out a bank deposit slip, the following steps guarantee an error-free submission process.

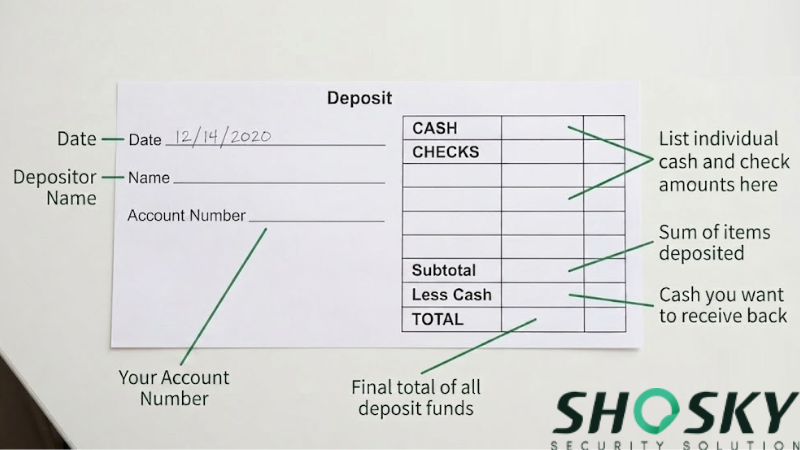

- Document Corporate Account Details: Enter your business name, account number, and the current date. This establishes the strict baseline for your audit trail.

- Endorse with For Deposit Only: Before listing checks, stamp or write “For Deposit Only” along with your business account number on the back of every check. This restricted endorsement heavily prevents theft if a check is dropped.

- Consolidate Physical Currency: Count your bills and coins. Enter the exact total of paper money on the “Cash” line and coins on the “Coin” line.

- List Serialized Checks Individually: List each check on its own line, entering the check number and the specific dollar amount. If you have more checks than lines, utilize the provided section on the back of the slip.

- Calculate the Subtotal: Add the cash, coins, and all listed checks together. Write this combined amount clearly on the “Subtotal” line.

- Declare Less Cash Received: If your business needs cash back from the deposit for register floats or petty cash, enter that exact amount on the “Less Cash Received” line.

- ign and Calculate Net Deposit: You only need to sign the signature line if you are requesting cash back in Step 6. Finally, subtract the cash back from your subtotal to calculate your “Total Net Deposit”.

Executing these steps helps maintain absolute accuracy and heavily reduces costly mistakes in commercial bank deposits. These specific details make it exceptionally easy for accounting departments to match physical cash with digital ledger records.

Securing Physical Transit: Clear vs Opaque Deposit Bags

Once you have completed your bank deposit slip and organized all your cash and checks, your job is only half finished. You must protect these liquid assets on the way to the banking facility.

Purchasing managers often debate whether to use transparent or opaque materials, but the choice depends entirely on your transit logistics.

| Evaluation Metrics | Clear Bags (Bank Standard) | Opaque Bags (Public Transit) |

|---|---|---|

| Primary Use Case | Night drops / Armored transport (CIT) | Retail staff walking or driving in public |

| Visibility | 100% Transparent (Contents visible) | 100% Blind (Contents hidden) |

| Security Focus | Internal audit & Liability protection | External deterrence & Theft prevention |

| Teller Verification | Instant verification before breaking seal | Requires breaking seal to verify contents |

| Key Advantage | Eliminates disputes over empty arrivals | Neutralizes opportunistic public targeting |

| Core Limitation | Exposes cash bundles to public view | Higher risk of internal counting disputes |

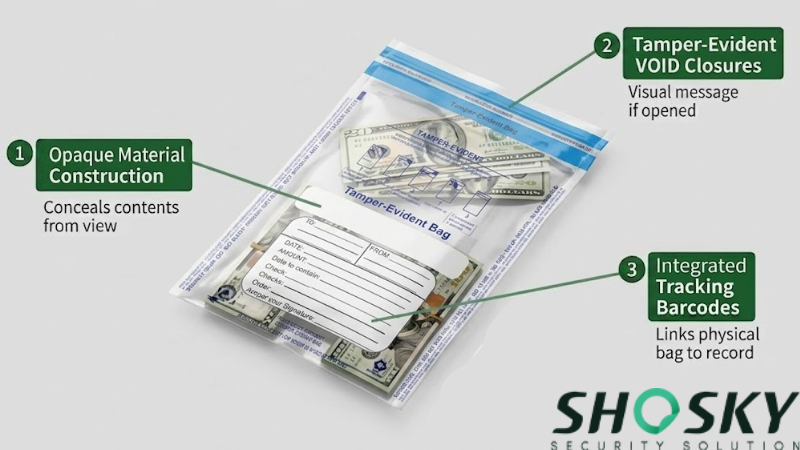

Regardless of opacity, professional security bags must always include these core engineering features:

- Tamper-Evident VOID Closures: Trigger a highly visible, irreversible VOID message if an unauthorized person attempts to open the bag before it reaches the secure banking facility.

- Integrated Tracking Barcodes: Links the physical cash bag directly to the digital paper deposit slip. This protocol satisfies strict corporate insurance policies and internal audit requirements.

Never carry loose corporate cash in a manila envelope or a generic plastic bag. Use a security bag designed specifically for high-risk deposits.

The integrated barcode gets scanned the exact moment you submit your deposit at the teller window, creating a permanent digital record that legally matches your paper form to the actual physical deposit. Keep your receipt from the teller and store it with your records.

Preventing Common Bank Deposit and Reconciliation Errors

Financial accuracy relies on dual control paired with a documented chain of custody. Shared responsibility during preparation helps reduce mistakes, while recorded handoffs keep each stage of the process traceable. Together, they lower the chance of internal errors or missing records.

The points below represent the first stage of financial protection. They focus on validation and control inside the organization before cash is transferred elsewhere.

| Error Type | How It Happens | How to Catch It |

|---|---|---|

| Transposition Errors | Numbers get accidentally swapped (like $500 becomes $005) | Compare your records to the bank statement line by line |

| Internal Skimming | One person handles the deposit without verification | Require two managers to sign off on the deposit slip |

| Missing Documentation | Deposits aren't recorded, or receipts get lost | Keep copies of all deposit slips for at least five years |

| Timing Delays | Funds don't appear in the account within the expected business day | Track submission dates and follow up with the bank if needed |

According to the Bank Secrecy Act (BSA) and regulations enforced by the Office of the Comptroller of the Currency (OCC), financial institutions and commercial businesses are highly advised to retain detailed records of transactions, including deposit slips, for a minimum of five years. Securing these physical copies alongside your digital tracking barcodes is essential for passing unexpected IRS or corporate audits.

Professional seals, security bags, and heavily labeled packaging protect your cash and deposit slips from unauthorized access and act as the ultimate final link in your chain of custody. They support perfectly clear tracking from retail collection to bank submission, eliminating the chance of interference or missing documentation.

Expert Tip from Shosky Security: Record the Bag Serial Number Before Sealing

The most common error in retail cash management occurs during the handoff. Before placing your cash and deposit slip into the tamper-evident bag and peeling the adhesive liner, permanently write the bag’s unique barcode serial number onto your internal corporate manifest ledger. If the bank ever reports a missing deposit, this matched serial number is the exact evidence your insurance company and local authorities will demand to initiate a tracking investigation.

FAQs

Why do commercial banks require tamper-evident deposit bags?

Commercial banks require tamper-evident deposit bags to establish a legally verifiable chain of custody. If the bag shows a triggered VOID message or physical damage upon arrival, the bank can immediately reject the deposit or initiate a fraud investigation, protecting both the financial institution and the corporate client from liability disputes.

What is the dual control process for bank deposits?

Dual control is an essential financial security protocol where two separate authorized employees must work together to count the cash, verify the check amounts, and sign the deposit slip. This method dramatically reduces the risk of internal skimming and accidental transposition errors before the funds are sealed for transit.

Can I use a regular envelope for my business deposit?

No. Using generic manila envelopes or standard plastic bags for corporate cash transit is highly dangerous. Standard envelopes lack sequential barcodes for digital tracking, opaque layers to hide cash from public view, and security closures that prove the funds were not accessed during transport to the bank.

What happens if the bank teller discovers a discrepancy on the deposit slip?

If the actual cash or check total inside the bag does not match the amount written on the deposit slip, the bank will pause processing and issue a credit or debit correction notice. Utilizing a serialized tamper-evident deposit bag ensures that any discrepancy is flagged as an administrative counting error rather than physical transit theft or internal tampering.

Upgrade Cash Transit Security Using Shosky Security Solutions

A deposit slip remains a key part of structured banking for businesses handling regular cash, checks, and mixed deposits. When filled out correctly, it helps align every deposit with the right bank account, reduces errors in transaction records, and keeps reconciliation smooth at the end of each business day.

For businesses looking to strengthen their deposit handling and cash transit security, Shosky Security offers tamper-evident bags, seals, and labeling solutions designed to protect bank deposits from handling errors and interference. Contact us to explore our secure packaging options and upgrade the way your deposits move from desk to bank.